Abraham Germansky was a multimillionaire real estate developer in 1920s. He also loved stocks, betting heavily as the market boomed. As the crash of 1929 unfolded, he was wiped out.

And that was basically the end of Abraham Germansky.

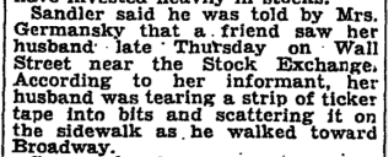

Germansky disappeared on October 24th, 1929. The New York Times posted a short story near the back of its October 26th edition, with Germansky’s lawyer, Bernard Sandler, asking for information on his whereabouts. It tells a powerful story in just a few words:

And that was basically the end of Abraham Germansky.

Germansky disappeared on October 24th, 1929. The New York Times posted a short story near the back of its October 26th edition, with Germansky’s lawyer, Bernard Sandler, asking for information on his whereabouts. It tells a powerful story in just a few words:

Later that week another investor in the same city had a very different experience.

Jesse Livermore returned home on October 29th to a wife who, seeing news of the day’s record market crash, was prepared to console her husband and return to a life of frugality.

Jesse said that wasn’t necessary. He was short the market and made more money in the crash of 1929 than during the rest of his life combined.

“You mean we are not ruined?” his wife asked, according to Livermore’s biography.

He replied: “No darling, I have just had my best ever trading day – we are fabulously rich and can do whatever we like.” He made, in one day, the equivalent of $3 billion.

Polar opposite stories. Germansky went broke, Livermore became the richest man in the world.

But fast-forward four years and the stories end up nearly identical.

Livermore made larger and larger bets, and went on to lose everything in the stock market. Broke and ashamed, he disappeared for two days in 1933. His wife set out to find him. “Jesse L. Livermore, the stock market operator, of 1100 Park Avenue missing and has not been seen since 3pm yesterday,” the New York Times wrote in 1933. He returned, but his path was set. Livermore eventually took his own life.

The timing was different, but Germansky and Livermore shared the realization that getting rich is one thing. Staying rich is quite another.

Everything in the economy is cyclical. Nothing great or terrible is likely to stay that way for long, because the same forces that cause things to be great or terrible also plant the seeds to push them the other way.

Bull markets make stocks expensive, expensive stocks leave little room for error, and little room for error increases the odds of bull markets ending. Same thing in the other direction. Recessions cause pessimism. Pessimism causes underproduction, underproduction leads to scarcity, scarcity leads to a new boom.

People and companies, whose behaviors are changed by their own success, are vulnerable to the same cycles.

I’ve noticed a pattern: Getting rich can be the biggest impediment to staying rich.

It goes like this. The more successful you are at something, the more convinced you become that you’re doing it right. The more convinced you are that you’re doing it right, the less open you are to change. The less open you are to change, the more likely you are to tripping in a world that changes all the time.

There are a million ways to get rich. But there’s only one way to stay rich: Humility, often to the point of paranoia. The irony is that few things squash humility like getting rich in the first place.

It’s why the composition of Dow Jones companies changes so much over time, and why the Forbes list of billionaires has 60% turnover per decade.

Andy Grove, Intel’s founder, put it this way: “Business success contains the seeds of its own destruction.” Scrappiness and the ability to think differently turns into complacency and the desire to keep things the same. Harvard Business Review wrote about Grove’s management philosophy in 1996:

Jesse Livermore returned home on October 29th to a wife who, seeing news of the day’s record market crash, was prepared to console her husband and return to a life of frugality.

Jesse said that wasn’t necessary. He was short the market and made more money in the crash of 1929 than during the rest of his life combined.

“You mean we are not ruined?” his wife asked, according to Livermore’s biography.

He replied: “No darling, I have just had my best ever trading day – we are fabulously rich and can do whatever we like.” He made, in one day, the equivalent of $3 billion.

Polar opposite stories. Germansky went broke, Livermore became the richest man in the world.

But fast-forward four years and the stories end up nearly identical.

Livermore made larger and larger bets, and went on to lose everything in the stock market. Broke and ashamed, he disappeared for two days in 1933. His wife set out to find him. “Jesse L. Livermore, the stock market operator, of 1100 Park Avenue missing and has not been seen since 3pm yesterday,” the New York Times wrote in 1933. He returned, but his path was set. Livermore eventually took his own life.

The timing was different, but Germansky and Livermore shared the realization that getting rich is one thing. Staying rich is quite another.

Everything in the economy is cyclical. Nothing great or terrible is likely to stay that way for long, because the same forces that cause things to be great or terrible also plant the seeds to push them the other way.

Bull markets make stocks expensive, expensive stocks leave little room for error, and little room for error increases the odds of bull markets ending. Same thing in the other direction. Recessions cause pessimism. Pessimism causes underproduction, underproduction leads to scarcity, scarcity leads to a new boom.

People and companies, whose behaviors are changed by their own success, are vulnerable to the same cycles.

I’ve noticed a pattern: Getting rich can be the biggest impediment to staying rich.

It goes like this. The more successful you are at something, the more convinced you become that you’re doing it right. The more convinced you are that you’re doing it right, the less open you are to change. The less open you are to change, the more likely you are to tripping in a world that changes all the time.

There are a million ways to get rich. But there’s only one way to stay rich: Humility, often to the point of paranoia. The irony is that few things squash humility like getting rich in the first place.

It’s why the composition of Dow Jones companies changes so much over time, and why the Forbes list of billionaires has 60% turnover per decade.

Andy Grove, Intel’s founder, put it this way: “Business success contains the seeds of its own destruction.” Scrappiness and the ability to think differently turns into complacency and the desire to keep things the same. Harvard Business Review wrote about Grove’s management philosophy in 1996:

Grove believes that at least some fear is healthy—especially in organizations that have had a history of success. Fear can be a healthy antidote to the complacency that success often breeds. A touch of paranoia—a suspicion that the world is changing against you—is what Grove prescribes.

Michael Moritz, the billionaire head of Sequoia Capital, was asked by Charlie Rose why Sequoia was so successful. Moritz mentioned longevity, noting that some VC firms succeed for five or ten years, but Sequoia has prospered for four decades. Rose asked why that was:

Moritz: I think we’ve always been afraid of going out of business.

Rose: Really? So it’s fear? Only the paranoid survive?

Moritz: There’s a lot of truth to that … We assume that tomorrow won’t be like yesterday. We can’t afford to rest on our laurels. We can’t be complacent. We can’t assume that yesterday’s success translates into tomorrow’s good fortune.

Not skill, or market insight, or even hard work. Fear and humility.

Humility doesn’t mean taking fewer risks. Sequoia takes as big of risks today as it did 30 years ago. But it’s taken risks in new industries, with new approaches, and new partners, cognizant that work worked yesterday isn’t what will work tomorrow.

IBM and Xerox did this when they shifted from hardware to services. Netflix did it when it cannibalized its DVD business to invest in streaming. GE has reinvented itself about every 20 years for the last century, going from a lightbulb company to a dishwasher company to a bank to a wind turbine company.

Each could have looked at their past success and concluded they were doing the right thing, patting themselves on the back. But they didn’t. They were, for the most part, paranoid, eager and willing to jettison past success in an attempt to keep up with where the world was heading next.

It’s not easy to do.

For decades people used Coke, Gillette, and American Express as examples of companies whose success was so solidified – whose moats were so deep and protected – that you could foresee their dominance indefinitely. But now all three are under attack. Coke’s is fighting 13 consecutive years of soda decline. Dollar Shave Club came out of nowhere to take 14 percentage points of market share away from Gillette. And as Charlie Munger, one of AmEx’s largest investors said this week: “If you think you know what the state of the payments system will be 10 years out you’re in a state of delusion.” Only the paranoid survive.

We don’t know much about Abraham Germansky – only that he went from rich, to broke, to disappeared. But we know a lot about Livermore, whose life was well documented.

Livermore was was one of the most skilled people in the world at getting rich. But few people in the early 20th century had a harder time staying rich. He made and lost at least four fortunes, never going more than eight years without flirting with bankruptcy.

After his third wipeout, Livermore recognized his mistake: Getting rich made him feel invincible, and feeling invincible led him to double-down with leverage on what worked in the recent past, which was catastrophic when the world changed and the market turned against him.

He reflected:

Humility doesn’t mean taking fewer risks. Sequoia takes as big of risks today as it did 30 years ago. But it’s taken risks in new industries, with new approaches, and new partners, cognizant that work worked yesterday isn’t what will work tomorrow.

IBM and Xerox did this when they shifted from hardware to services. Netflix did it when it cannibalized its DVD business to invest in streaming. GE has reinvented itself about every 20 years for the last century, going from a lightbulb company to a dishwasher company to a bank to a wind turbine company.

Each could have looked at their past success and concluded they were doing the right thing, patting themselves on the back. But they didn’t. They were, for the most part, paranoid, eager and willing to jettison past success in an attempt to keep up with where the world was heading next.

It’s not easy to do.

For decades people used Coke, Gillette, and American Express as examples of companies whose success was so solidified – whose moats were so deep and protected – that you could foresee their dominance indefinitely. But now all three are under attack. Coke’s is fighting 13 consecutive years of soda decline. Dollar Shave Club came out of nowhere to take 14 percentage points of market share away from Gillette. And as Charlie Munger, one of AmEx’s largest investors said this week: “If you think you know what the state of the payments system will be 10 years out you’re in a state of delusion.” Only the paranoid survive.

We don’t know much about Abraham Germansky – only that he went from rich, to broke, to disappeared. But we know a lot about Livermore, whose life was well documented.

Livermore was was one of the most skilled people in the world at getting rich. But few people in the early 20th century had a harder time staying rich. He made and lost at least four fortunes, never going more than eight years without flirting with bankruptcy.

After his third wipeout, Livermore recognized his mistake: Getting rich made him feel invincible, and feeling invincible led him to double-down with leverage on what worked in the recent past, which was catastrophic when the world changed and the market turned against him.

He reflected:

I sometimes think that no price is too high for a speculator to pay to learn that which will keep him from getting the swelled head. A great many smashes by brilliant men can be traced directly to the swelled head.

“It’s an expensive disease everywhere to everybody” he said.

Originally published on collaborativefund.com

RSS Feed

RSS Feed